Its already old AF its on a southwest aspect does not get big. I have lived next to it since 1986. This stuff does not add up.

I will add the polygon into the structures wtf is that from?

I want to see the science

Its already old AF its on a southwest aspect does not get big. I have lived next to it since 1986. This stuff does not add up.

I will add the polygon into the structures wtf is that from?

I want to see the science

It’s a tough challenge when our understanding of what is possible gets redefined every couple years.

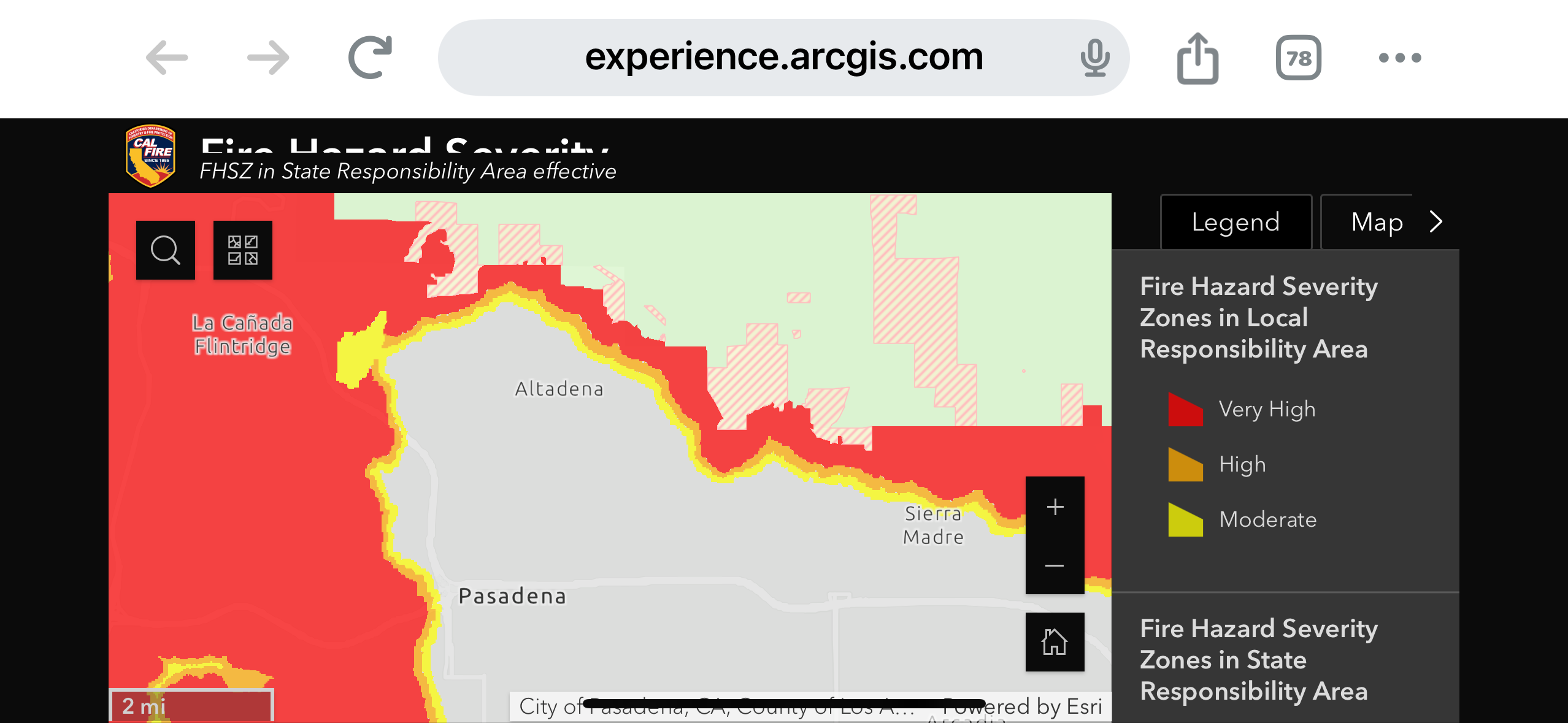

I mean they left out most of altadena. Their credibility is shot. Im gonna get the polygon and lay it over it.

I checked on one of my old first due areas that always had me saying man on windy day this area is gonna be a problem. You cant make this up. This is the reverse of me. Stuff that should probably be high or at a minimum moderate has no score.

Here is the google map link.

https://maps.app.goo.gl/HpkSMRcRKxqzKKVa6?g_st=com.google.maps.preview.copy

What sucks is the insurance companies will take this as gospel as its from the government.

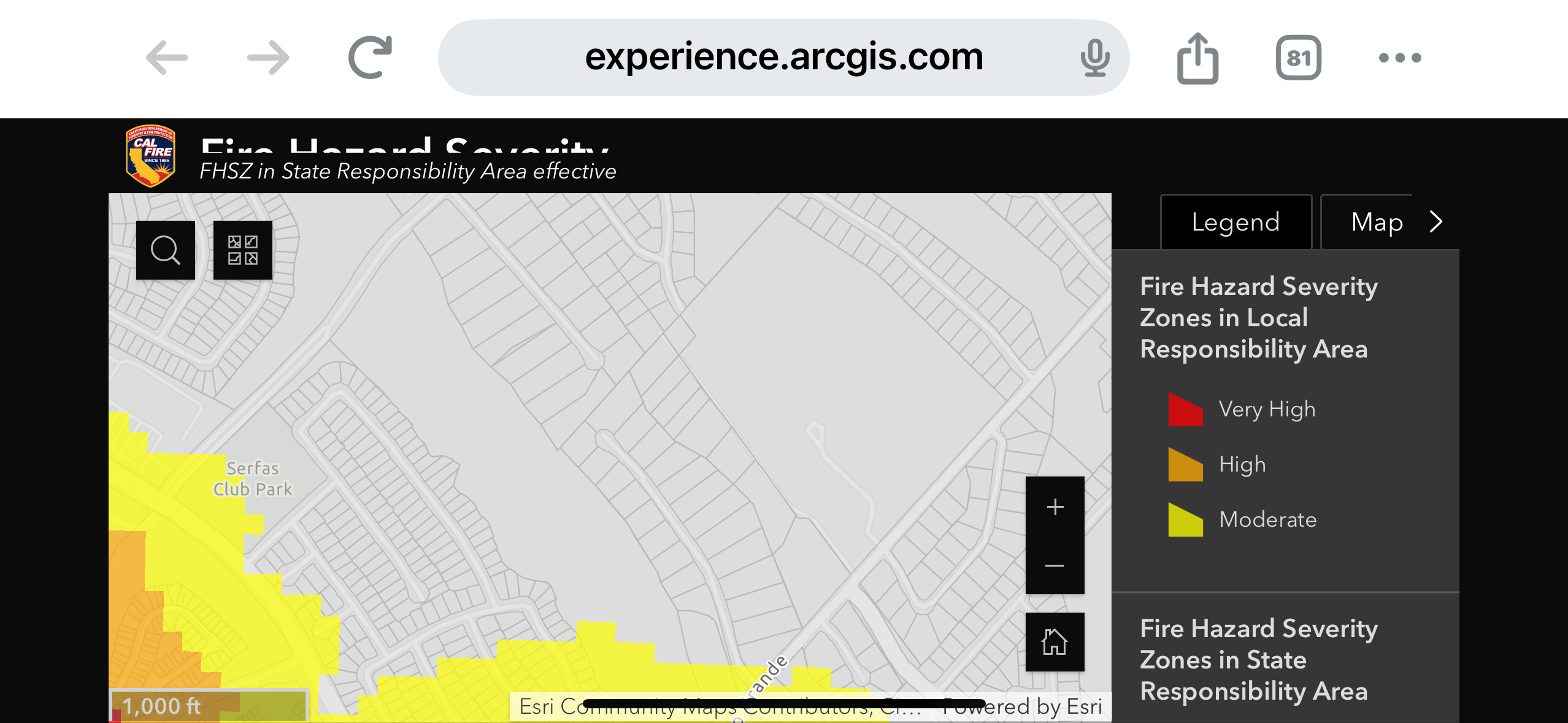

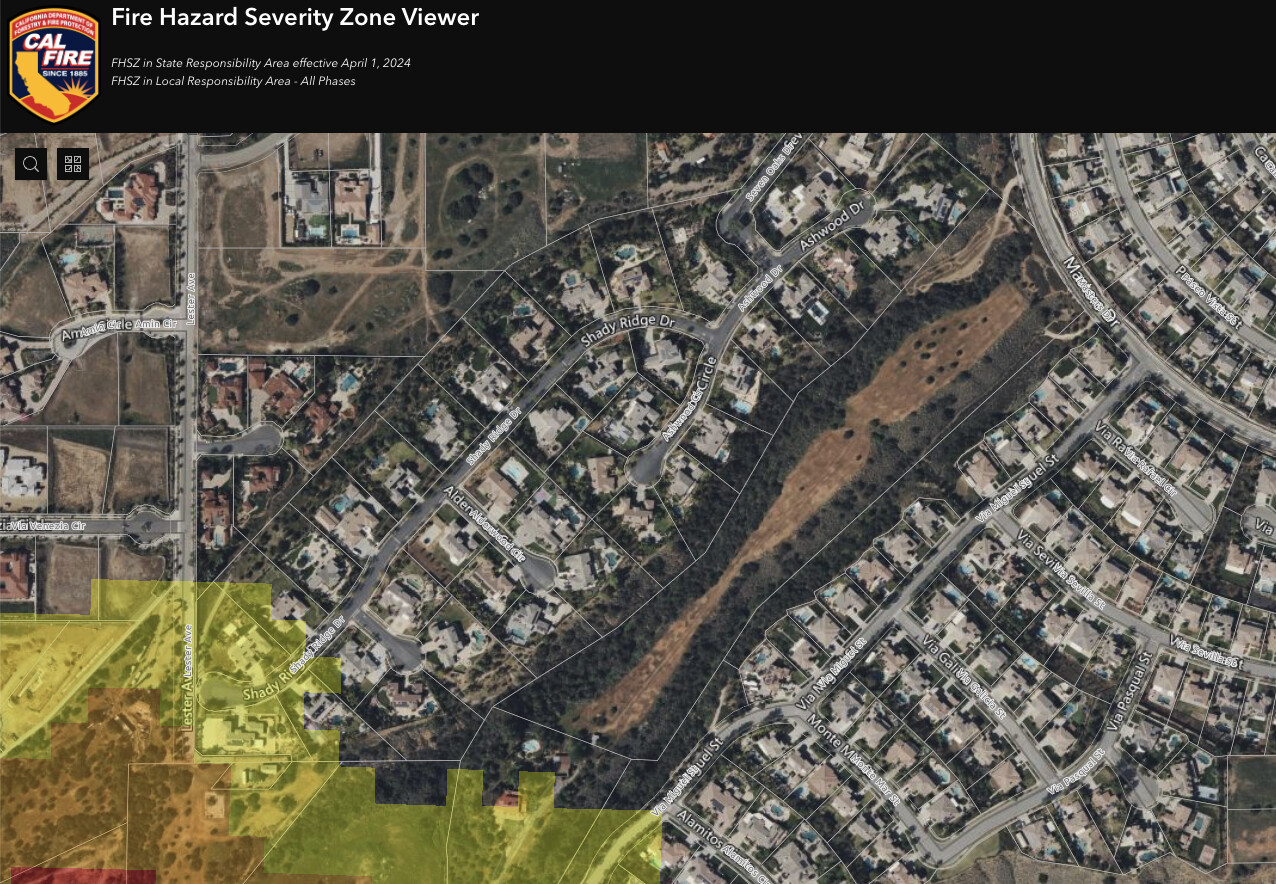

Sure would have made it easier if they had snapped to property lines. 95% of my 1/4 acre lot is in moderate. Bets on whether my insurance company sees the bit that is high?

@Fish you are spot. It is finger painting.

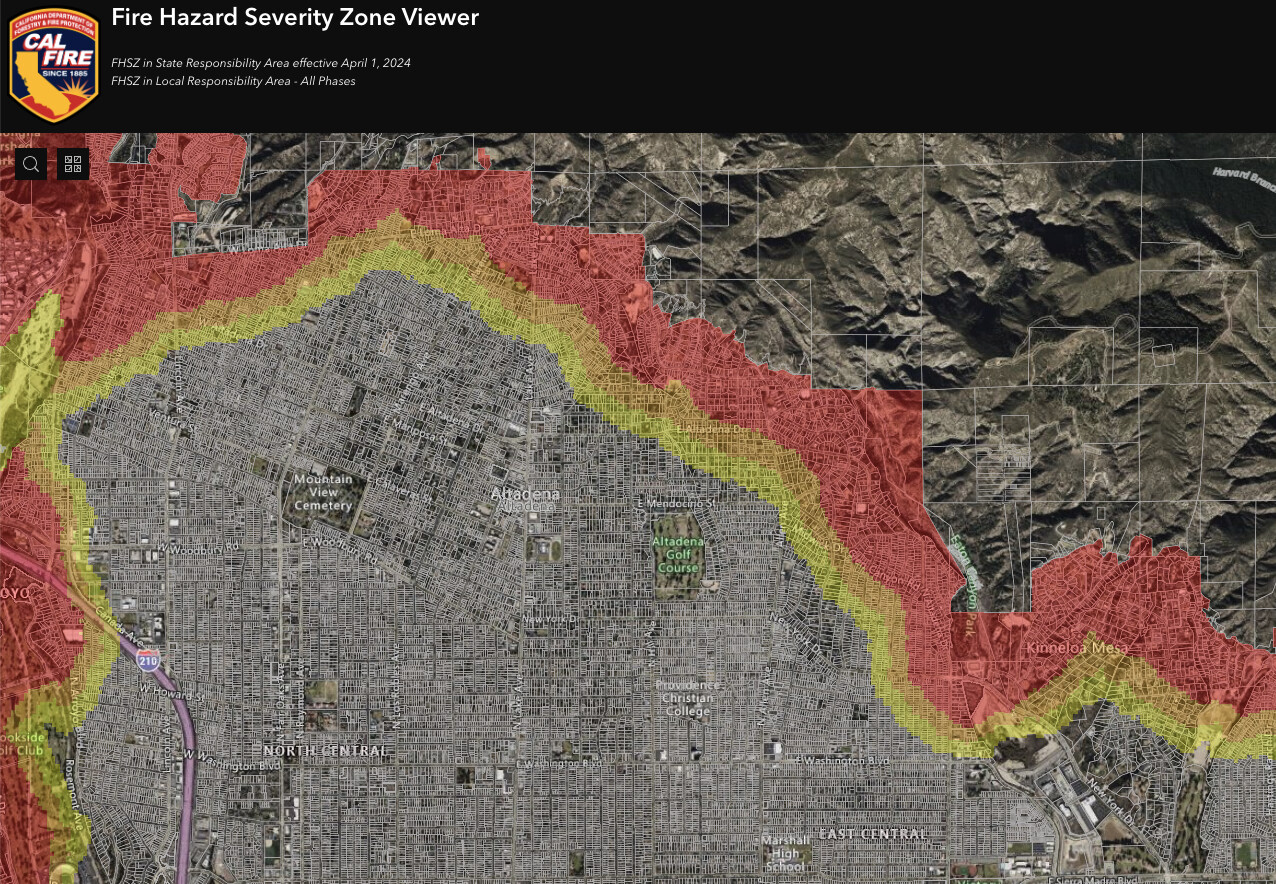

My favorite is the Altadena area. Come on we can do better than this.

Look at the buffer from the very high to high to moderate. Its just uniform.

So it seems to me there is painting with a pretty wide brush.

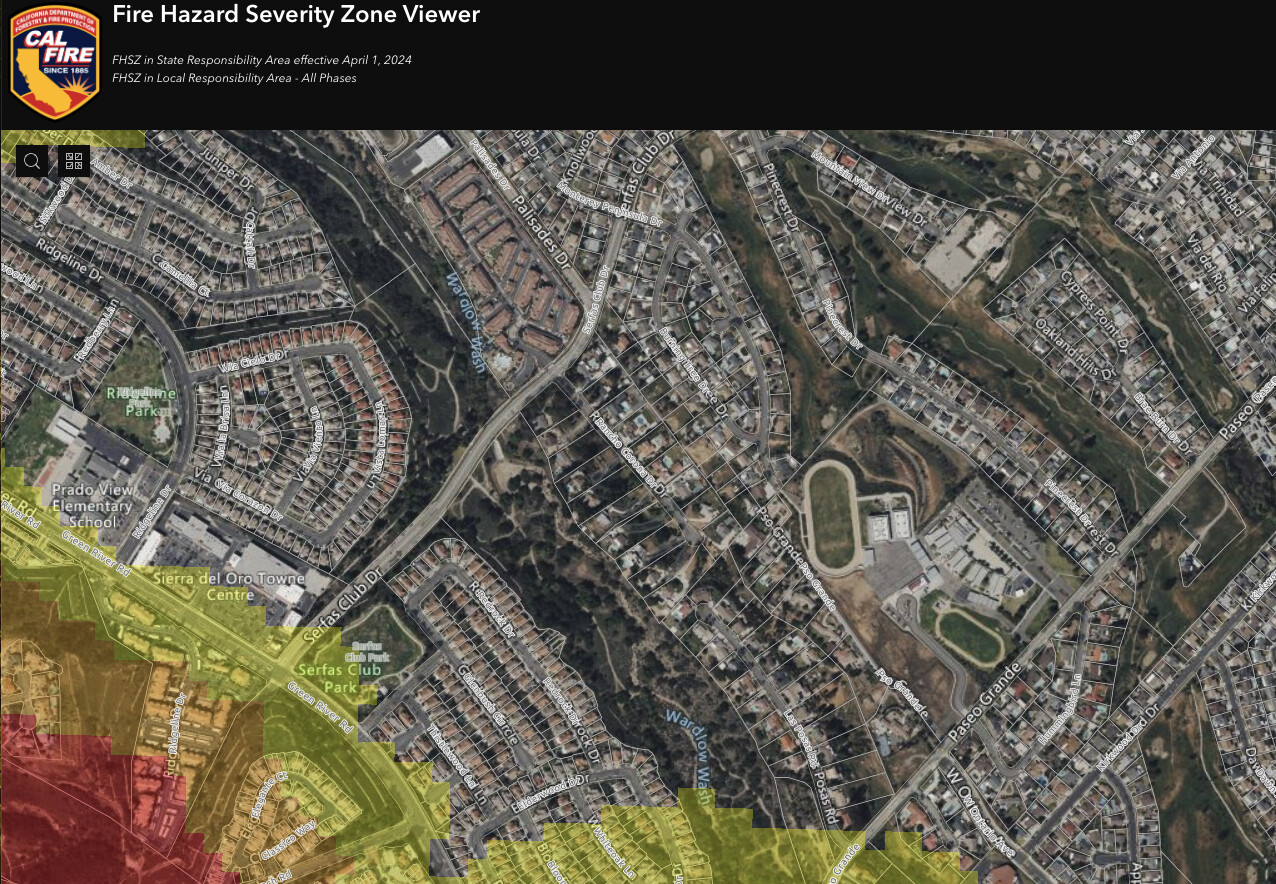

And then this so the fire hazard zone just stops? Continous fuel for a bit. If your gonna make a fire hazard zone map that is public put some science into it.

I did a little measuring at it appears like a 700 footish buffer between the edge of the very high to the high and same from high to end of moderate and then it ends.

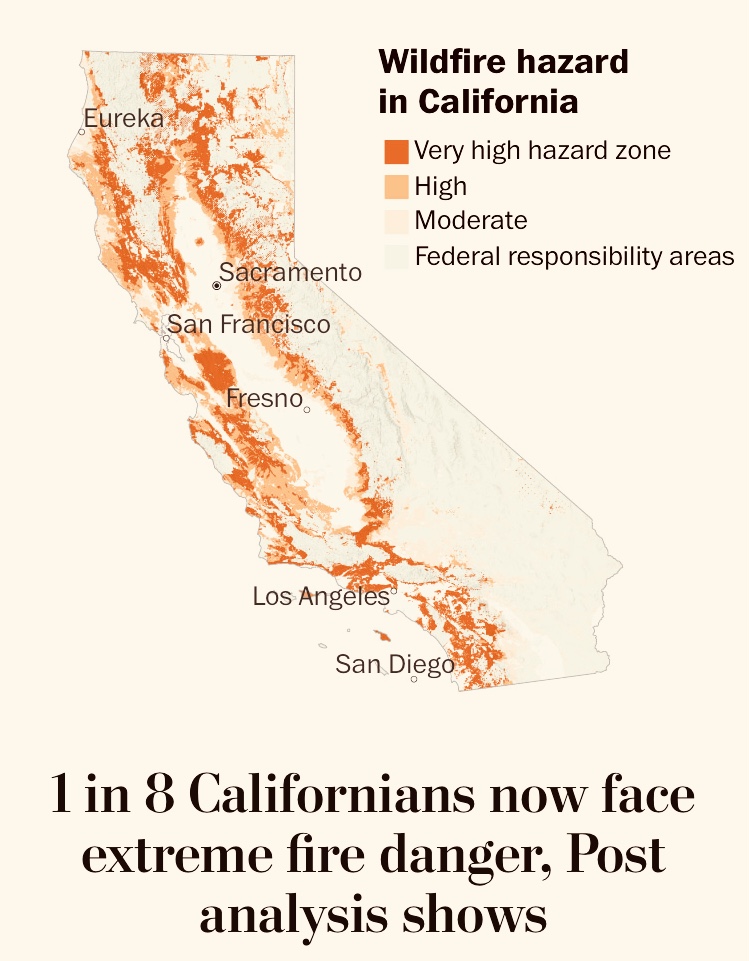

One thing for sure this is going to change the Real Estate Housing Market. Throwing another Ten Grand if not more to your mortgage every year is going to hurt. If you rent a single family or multi family dwelling in these areas, I would think the rents are going up. Just the tip of the iceberg. So what happens to the housing market in these affected areas. Housing prices going down? Crazy times all around. I had to move a bunch of my insurance around to get a better deal on my house. But from what happen down south and the new maps that just came out. I’m planning on Fair Plan coverage next go around. I just renewed my insurance a month before the fire down south. I am expecting a letter saying the will not renew my coverage.

Simple answer

Total collapse and locking up of the market.

Nobody will be able to afford the Fire and/or Mortgage Insurance. If you have say a $500,000.00 home and the only thing available is FAIR PLAN. That only covers 75%. So on top of the 20% down payment. You’ll also be required to have the difference between the FAIR PLAN and the amount of the mortgage. How many people will have $100k for the 20% down and another 100k to make up the difference in insured value?

Let’s not forget, the FAIR PLAN is already upside down and is seeking a 50% increase in premiums to make up for the insured losses and keep the program from becoming insolvent.

Finally, if/when the market does collapse and said $500,000 house that has property taxes at 1.75% of assessed value is only now worth $250,000.00 the property owner is going to get a reassessment from the county assessor like what happened from 2007-2012. Their will only crater the LG tax base which in turn, put increased pressure on LG budgets. Last time this happened PERS went from high 70% range funding to high 60% range funding.

This cascading event will have the potential to do what the GREAT RECESSION didn’t do, bring down entire state governments.

Who else beside California has this problem ?

Colorado now facing the same

Let’s see what could be the problem. State Farm General (the CA subsidiary of State Farm Mutual) funnels a bunch of their money to their parent company State Farm Mutual. State Farm Mutual declares record profits last year. State Farm General say we need to raise rates to stay viable. State Farm Mutual say were not going to help State Farm General financially.

That’s it, peoples rates need to be raised.

States are sovereign, they can’t be “brought down”. They can however cut services if their constituents do not want to tax themselves to provide those services. Though that borders on a distinction without a difference to the average joe.

Where does the fire risk on FRA lands fall into this map ? Is there a similar map made for fed lands ?

People dont live on Fed lands so i dont think there is a hazard map directed in that fashion.

There are cabins in national forests surrounded by federal land . Wondering if there is a federal hazard map that insurance uses. These properties don’t show up on the state map.

Ok yeah leased cabins but its probably 0.00001 of all homes in CA. When it burns down I doubt they will let you rebuild. The insurance is probably just a pay out to you.

Hurricane prone states are having similar issues. Florida, TX and Alabama are experiencing the exact same issues with policy rates and cancelations.

It is too bad when two of the governors from two of the states that are having the issues got together for a debate… missed the opportunity to work together to solve the problem by finding commonality.

There are places within CA where insurance is being canceled because of building density… these are not in or near where it would be considered WUI. This has to do with post earthquake fires.

Not sure it would bring a state down. It will further the housing bubble. The people at PERS are pretty good at what they do.